When it comes to buying and selling property, timing is often critical. Having to wait while an existing property sells before buying a new one can mean missing out on the ideal property or buying in a favourable market. One solution for homeowners and property investors is bridging finance: a short-term loan that bridges the financial gap between the sale of an existing property and the purchase of a new one.

What is a bridging loan?

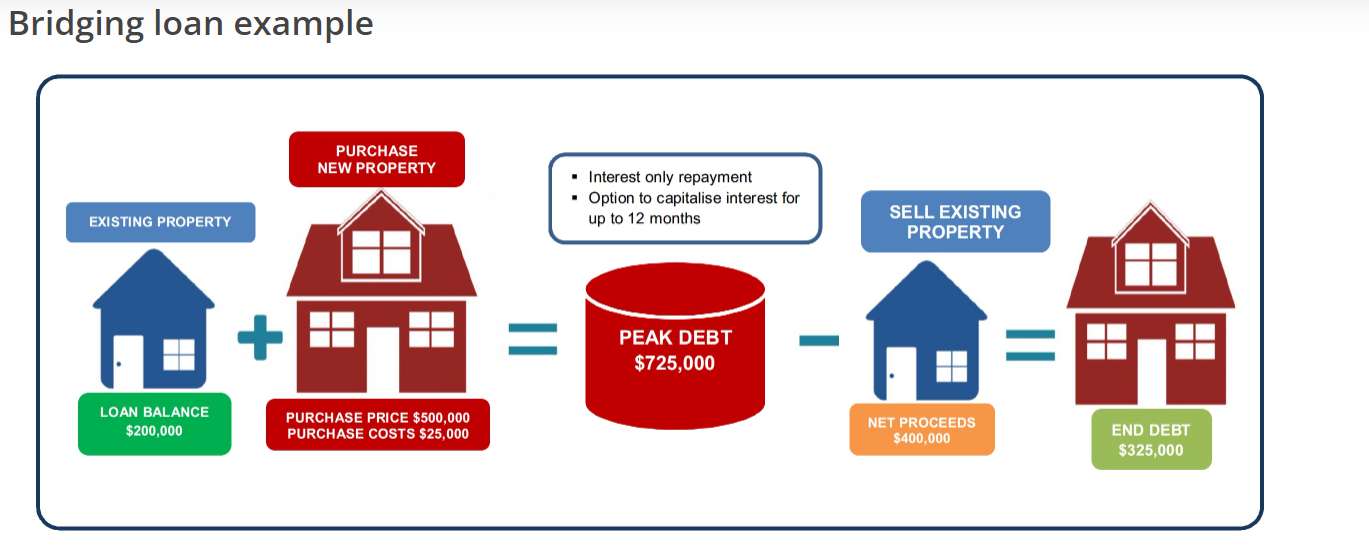

Bridging loans are short-term loans used by homeowners and property investors to finance the purchase of a new property before an existing one is sold. Typically, a bridging loan:

- Is a separate loan to an existing mortgage.

- Is an interest-only home loan.

- Has a value that is calculated according to the equity in the existing property.

- Has a limited loan term, typically up to 12 months.

- Carries special conditions, such as a lender being able to charge a higher interest rate if the property is not sold within a certain timeframe.

- Is structured differently and varies from lender to lender.

When deciding whether a bridging loan is the right option, homeowners must be certain they can meet the repayments on both the existing loan and the bridging loan.

Although many lenders don’t require repayments on the bridging loan within the bridging period, the interest is capitalised up to the loan term and added to the loan balance, which means borrowers pay interest on this interest.

Some lenders allow borrowers to make extra repayments into their bridging loan, but typically there is no access to a redraw facility, so borrowers are unable to access these funds later.

Before choosing bridging finance, it’s important to have a sound understanding of the property market, to be confident that the existing property will sell and that the bridging loan can be repaid within the agreed term.

Not selling before the bridging period ends will mean making repayments on both the existing home loan and the new home loan, while selling the existing property for less than expected, could leave borrowers with a higher loan balance than anticipated.

Benefits of bridging loans

Seamless property transactions

Bridging finance helps ensure a smooth transition between buying a new home and selling an existing one. That’s especially helpful in a buyer’s market when properties are in high demand, as it allows borrowers to move quickly to buy the ideal home.

Repayment flexibility

Depending on the loan type, bridging finance typically offers flexible repayment options, giving borrowers the freedom to choose between interest-only payments during the bridging period or making principal and interest repayments.

Minimal disruption

By using bridging finance, homeowners avoid the inconvenience of moving twice or needing to find temporary accommodation between property transactions, providing a seamless transition without the need to uproot their lives temporarily.

Risks of bridging loans

Financial risk

The biggest risk for homeowners is that repayment of the bridging loan relies on the sale of the existing property. If the sale falls through or takes longer than anticipated, borrowers may find themselves facing financial strain as they may be required to service two loans simultaneously.

Interest costs

Bridging finance often carries higher interest rates compared to traditional home loans, so it's essential that homeowners carefully evaluate the costs involved, including interest charges and fees, to ensure that the benefits outweigh the additional expense.

When to consider bridging finance?

Bridging finance may be suitable for homeowners who are considering:

- Upsizing or Downsizing

- Buying at auction

- Investing in property

- Renovating their existing home

Is bridging finance right for you?

Bridging finance can be an effective solution for homeowners in Australia looking for a seamless transition between buying a new home and selling an existing one.

While the ability to move quickly and put in an offer on a new home is a significant advantage, homeowners should carefully assess the financial impact that this type of financing could have on their financial situation.

For expert advice around bridging finance and bridging loans in Australia, contact a Mortgage Express finance consultation today.

While all care has been taken in the preparation of this publication, no warranty is given as to the accuracy of the information and no responsibility is taken by Finservice Pty Ltd (Mortgage Express) for any errors or omissions. This publication does not constitute personalised financial advice. It may not be relevant to individual circumstances. Nothing in this publication is, or should be taken as, an offer, invitation, or recommendation to buy, sell, or retain any investment in or make any deposit with any person. You should seek professional advice before taking any action in relation to the matters dealt within this publication. A Disclosure Statement is available on request and free of charge.

Finservice Pty Ltd (Mortgage Express) is authorised as a corporate credit representative (Corporate Credit Representative Number 397386) to engage in credit activities on behalf of BLSSA Pty Ltd (Australian Credit Licence number 391237) ACN 123 600 000 | Full member of MFAA | Member of Australian Financial Complaints Authority (AFCA) | Member of Choice Aggregation Services.